Understanding how these payments are structured and taxed can make a difference in planning your finances and making informed decisions.

DVA Payments that are usually taxed

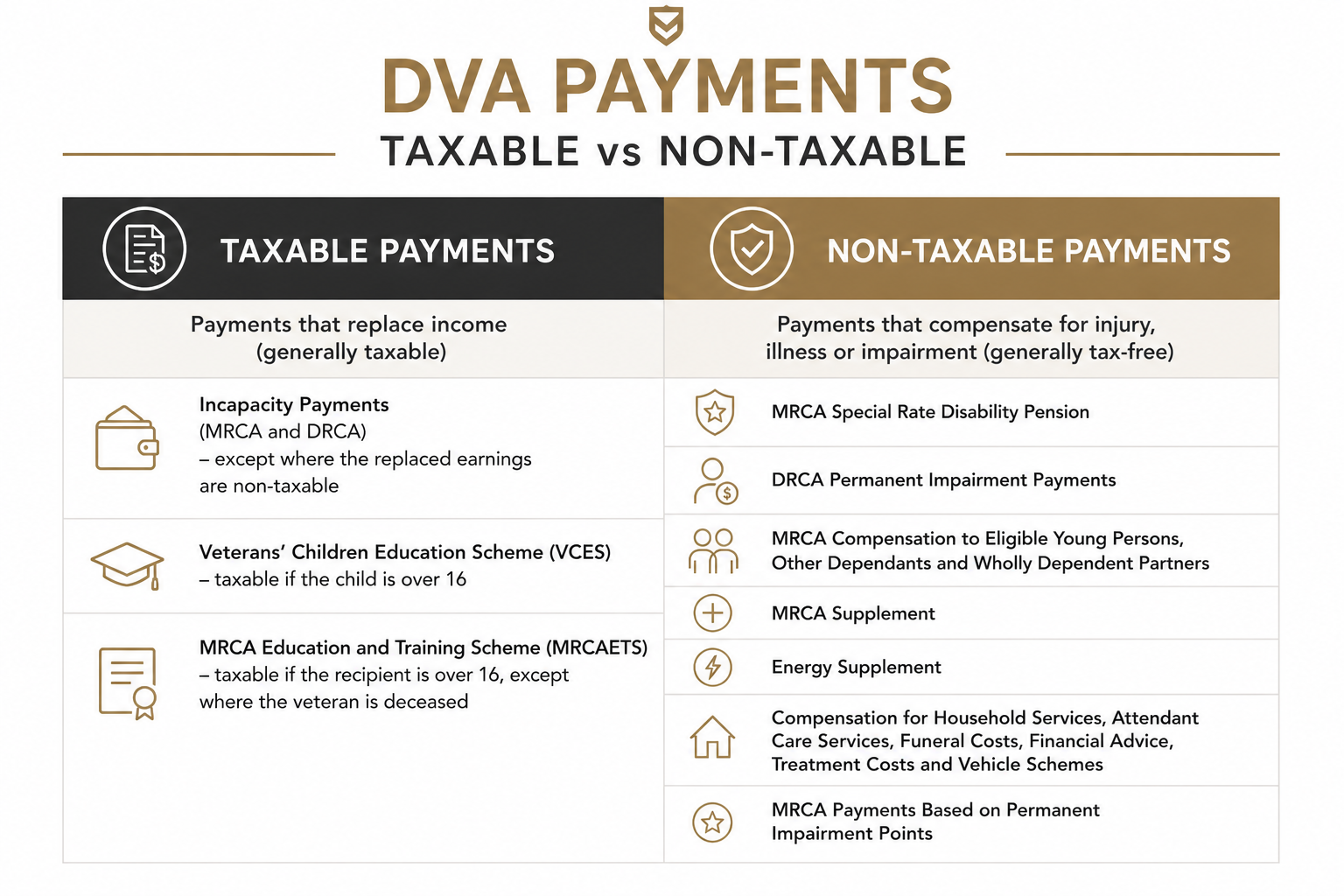

The following payments are generally considered income support or income replacement and are taxable.

Incapacity Payments (MRCA)

Incapacity payments under MRCA are designed to replace income where your ability to work is affected by a service-related condition. They are based on the difference between what you would have earned and what you are able to earn, and are taxable. In some cases, they may be tax-free where the earnings being replaced were also non-taxable.

Incapacity Payments (DRCA)

Incapacity payments under DRCA provide income support where a service-related injury or illness impacts your capacity to work. These payments are typically based on your pre-injury earnings and are taxable. In some cases, they may be tax-free where the earnings being replaced were also non-taxable.

Service Pension

The Service Pension is a regular income support payment for eligible veterans. Service Pension (Age) is generally taxable, except for any supplementary tax-exempt amount. Service Pension (Invalidity) may be tax-free if you are under the Social Security Age Pension age, but it may become taxable once you reach that age.

Income Support Supplement

The Income Support Supplement payment is generally treated as income support and may be taxable, although exemptions can apply in some incapacity-related circumstances.

Veteran Payment

The Veteran Payment is a short-term income support payment available while a claim is being assessed. The main component of Veteran Payment is generally taxable, although certain supplementary components may not be.

Education and Training Payments (Conditional)

Some veterans or dependants may be eligible for payments to assist with the cost of education. Payments under the Veterans’ Children Education Scheme (VCES) and the MRCA Education and Training Scheme (MRCAETS) may be taxable depending on who receives the payment and their circumstances.

Payments under the Veterans’ Children Education Scheme and the MRCA Education and Training Scheme depend on the student’s age and the type of payment. Payments made to students under 16 are generally tax-free. Education allowances paid to students aged 16 or over are generally taxable, while supplementary payments such as special financial assistance and additional tuition are generally tax-free. Exceptions can also apply to some MRCAETS payments made following a veteran’s death.

DVA Payments That Are Generally Tax-Free

Many DVA compensation payments are not taxable where they are designed to compensate for the impact of service-related injury, illness, impairment, or death.

Permanent Impairment (PI) Payments (MRCA & DRCA)

Permanent impairment compensation under the MRCA and DRCA is generally tax-free because it compensates for permanent impairment arising from an accepted service-related injury or disease. Under MRCA, payments may be taken periodically, as a lump sum, or in some cases as a combination. Understanding how to manage a lump sum payment is an important part of making an informed financial decision.

Veterans’ Entitlements Act (VEA) Disability Pension

Disability Compensation Payments (previously known as the Disability Pension) under the Veterans’ Entitlements Act are generally tax-free, as they are paid to compensate for the impact of service-related conditions rather than to replace income.

Special Rate Disability Pension (SRDP)

The Special Rate Disability Pension under the Military Rehabilitation and Compensation Act 2004 is generally tax-free. Although it is paid on an ongoing basis, it is classified as compensation for severe impairment rather than income replacement.

Compensation to Dependants

Compensation payments made to eligible dependants under the Military Rehabilitation and Compensation Act 2004 (MRCA) are generally tax-free. These payments are designed to compensate for the impact of a service-related injury or death, rather than to provide taxable income.

This may include compensation paid to:

- Wholly dependent partners – such as a spouse or de facto partner who was financially dependent on a veteran who died due to a service-related condition.

- Eligible young persons – including dependent children who may receive support while completing approved education or training.

- Other dependants – in some circumstances, compensation may also be paid to family members who were financially dependent on the veteran.

Because these payments are compensatory in nature rather than income-replacement, they are generally not taxed.

Household Services and Attendant Care

Household Services payments that cover the cost of domestic assistance, personal care, and support services are not considered income and are generally tax-free.

Medical and Treatment Benefits

DVA-funded medical treatment, rehabilitation services, and healthcare-related benefits are not taxable.

Funeral and Bereavement Payments

Payments made to assist with funeral costs or to support dependants following a veteran’s death are generally tax-free.

Energy Payments

The Energy Supplement is a non-taxable payment provided to help with energy costs. It is paid in addition to certain DVA benefits and does not need to be included as taxable income.

Vehicle Schemes

Vehicle schemes may provide assistance with vehicle modifications or transport support for veterans whose accepted service-related conditions significantly affect mobility. These benefits are generally tax-free as they are compensatory in nature.

War Widow/Widower and Orphan Pensions

The War Widow or Widower Pension under the Veterans’ Entitlements Act 1986 (VEA) is generally tax-free and is not treated as assessable income for tax purposes. This pension is paid to eligible spouses or partners where the veteran’s death was related to qualifying or operational service, or where other eligibility criteria are met.

Orphan pensions paid to eligible dependent children of deceased veterans are also generally tax-free. These payments are designed to provide financial support to children affected by the loss of a parent due to service-related death.

MRCA Supplement

The MRCA Supplement is generally tax-free. It is a fortnightly payment for eligible MRCA claimants and replaces telephone, internet and pharmaceutical allowance support.

Financial Advice Payments

In some circumstances, veterans may be eligible for DVA financial advice reimbursement, particularly when required to make an important compensation decision, such as choosing between payment options for Permanent Impairment (PI) or SRDP. These payments are generally not taxable, as they are intended to support informed decision-making rather than provide income.

Understanding the Difference Between Compensation and Income

Most DVA payments arise from a service-related injury or illness. However, how those payments are treated for tax purposes does not depend on the condition but on what the payment compensates for.

Some payments, such as Permanent Impairment, recognise the long-term impact of a condition. These payments reflect the effect the condition has had on your life and not your ability to earn income.

Other payments are linked more directly to income, such as Incapacity payments, which are paid when your ability to work has been affected and are based on lost earnings.

The Special Rate Disability Pension often sits in between these two concepts. It is paid on an ongoing basis and is often associated with a reduced ability to work. Despite this, it is classified as compensation for severe impairment rather than a direct replacement of income, which is why it is generally not taxed.

The veteran compensation system in Australia is moving to a new structure from 1 July 2026, under the Vets Act 2025. Understanding how these changes affect you is important for protecting your financial future.

Tax-Free Payments Can Still Affect Tax Position

Even when a DVA payment is classified as tax-free, it does not mean there are no tax consequences. Tax-free payments are not taxed directly, but they may still affect your broader financial position, including eligibility for other benefits, offsets, concessions, or income-tested support.

In some cases, tax-free payments may be taken into account when assessing eligibility for other income-tested benefits or offsets. This can influence access to certain government support payments or concessions.

There can also be indirect effects when tax-free payments are received alongside taxable income. While the payment itself is not taxed, it may affect how other income is structured or influence planning decisions around superannuation, investments, or retirement income.

National Service Financial Can Help You Understand DVA Payments and Plan Around Tax

How DVA payments are taxed is rarely simple, especially when several payments are in play, or your circumstances shift over time. Many DVA compensation payments are tax-free, but others – particularly those designed to replace lost income – may be taxable. Treatment can also differ depending on whether a payment sits under MRCA, DRCA, or VEA.

Even tax-free payments matter to your wider financial position. The mix of taxable and non-taxable payments can affect your cash flow, your tax return outcomes, your eligibility for other benefits, and the income you have available over time. Reassessments, changes in circumstances, or moving between payment types can shift that picture again.

NSF has a strong working knowledge of how entitlements are taxed, and we use it to give you clarity on how your DVA payments are structured, how they’re treated, and how they interact with the rest of your finances. That said, tax planning itself is best done in consultation with your accountant alongside NSF – your accountant brings the details of your full tax position, and we bring the entitlements and financial-strategy lens. Together, that combination helps you make informed decisions and avoid unexpected outcomes.

National Service Financial advises current and former ADF members and their families – helping you understand your entitlements, navigate compensation decisions, and consider the financial and tax implications for your individual circumstances.

")